Over 2 million + professionals use CFI to learn accounting, financial analysis, modeling and more. Unlock the essentials of corporate finance with our free resources and get an exclusive sneak peek at the first module of each course. Start Free

In accounting, goodwill is an intangible asset . The concept of goodwill comes into play when a company looking to acquire another company is willing to pay a price premium over the fair market value of the company’s net assets.

The elements or factors that a company is paying extra for or that are represented as goodwill are things such as a company’s good reputation, a solid (loyal) customer or client base, brand identity and recognition, an especially talented workforce, and proprietary technology. These things are, in fact, valuable assets of a company. However, they are neither tangible (physical) assets nor can their value be precisely quantified.

Under US GAAP and IFRS Standards , goodwill is an intangible asset with an indefinite life and thus does not need to be amortized. However, it needs to be evaluated for impairment yearly, and only private companies may elect to amortize goodwill over a 10-year period.

Goodwill is sometimes separately categorized as economic, or business, goodwill and goodwill in accounting, but to speak as if these were two separate things is an artificial and misleading construct. What is referred to as “accounting goodwill” is really just the recognition in the accounting of a company’s “economic goodwill.”

Accounting goodwill is sometimes defined as an intangible asset that is created when a company purchases another company for a price higher than the fair market value of the target company’s net assets. But referring to the intangible asset as being “created” is misleading – an accounting journal entry is created, but the intangible asset already exists. The entry of “goodwill” in a company’s financial statements – it appears in the listing of assets on a company’s balance sheet – is not really the creation of an asset but merely the recognition of its existence.

Economic, or business, goodwill is defined as previously noted: an intangible asset – for example, strong brand identity or superior customer relations – that provides a company with competitive advantages in the marketplace. Both the existence of this intangible asset, as well as an indication or estimate of its value, is often drawn from examining a company’s return on assets ratio.

Warren Buffett used California-based See’s Candies as an example of this. See’s consistently earned approximately a two million dollar annual net profit with net tangible assets of only eight million dollars. Because a 25% return on assets is exceptionally high, the inference is that part of the company’s profitability was due to the existence of substantial goodwill assets.

The inference of contributing intangible assets was borne out as being based in fact, as See’s was widely recognized in the industry as enjoying a significant edge over its competitors by virtue of its overall favorable reputation and, specifically, thanks to its outstanding customer service relations.

The following excerpt from Warren Buffett’s 1983 Berkshire Hathaway shareholder letter explains and indicates the estimate of the value of goodwill:

“Businesses logically are worth far more than net tangible assets when they can be expected to produce earnings on such assets considerably in excess of market rates of return. The capitalized value of this excess return is economic goodwill.”

The journal entry is as follows:

Purchase of a Company:

To understand it in more depth, let’s look at an example.

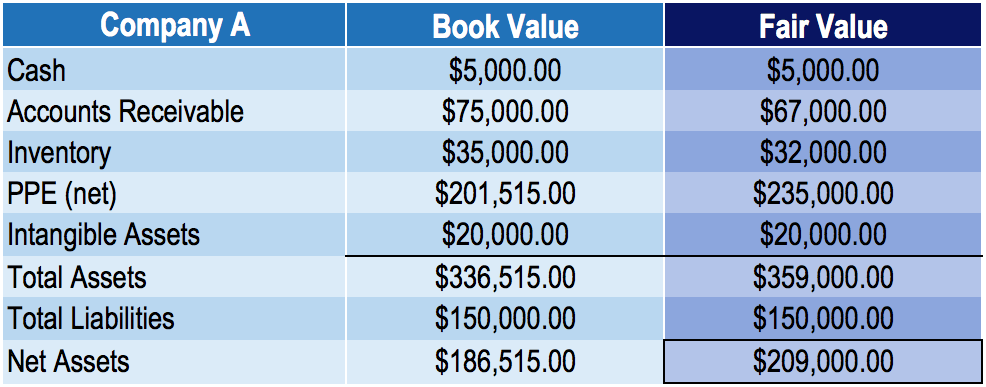

Company A reports the following amounts:

The fair value differs from book value in the example above because:

If Company B purchases Company A for $250,000, the amount of economic goodwill “created” would be the purchase price minus the fair market value of net assets: $250,000 – $209,000 = $41,000.

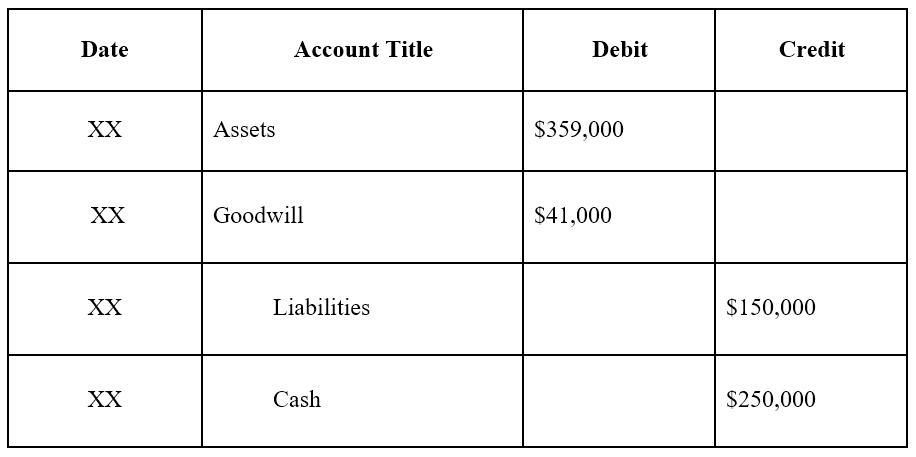

The journal entry for the purchasing company, Company B, would be as follows:

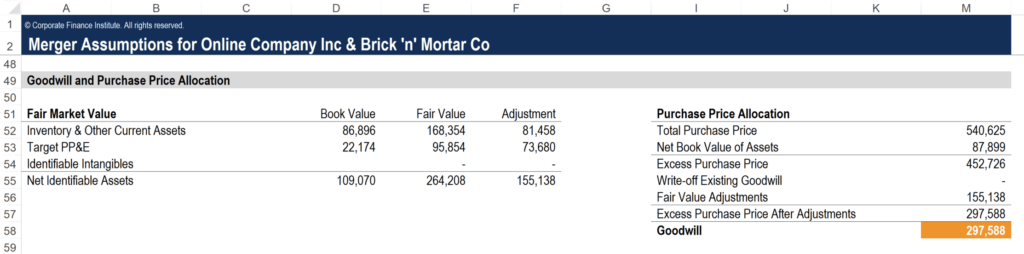

In financial modeling for mergers and acquisitions (M&A), it’s important to accurately reflect the value of goodwill in order for the total financial model to be accurate. Below is a screenshot of how an analyst would perform the analysis required to calculate the values that go on the balance sheet.

This screenshot is taken from CFI’s M&A Financial Modeling Course.

First, get the book value of all assets on the target’s balance sheet. This includes current assets, non-current assets, fixed assets, and intangible assets. You can get these figures from the company’s most recent set of financial statements.

Next, have an accountant determine the fair value of the assets. This process is somewhat subjective, but an accounting firm will be able to perform the necessary analysis to justify a fair current market value of each asset.

Calculate the adjustments by simply taking the difference between the fair value and the book value of each asset.

Next, calculate the Excess Purchase Price by taking the difference between the actual purchase price paid to acquire the target company and the Net Book Value of the company’s assets (assets minus liabilities).

With all of the above figures calculated, the last step is to take the Excess Purchase Price and deduct the Fair Value Adjustments. The resulting figure is the Goodwill that will go on the acquirer’s balance sheet when the deal closes.

Thank you for reading CFI’s guide to Goodwill. To help you advance your career, check out the additional CFI resources below:

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.